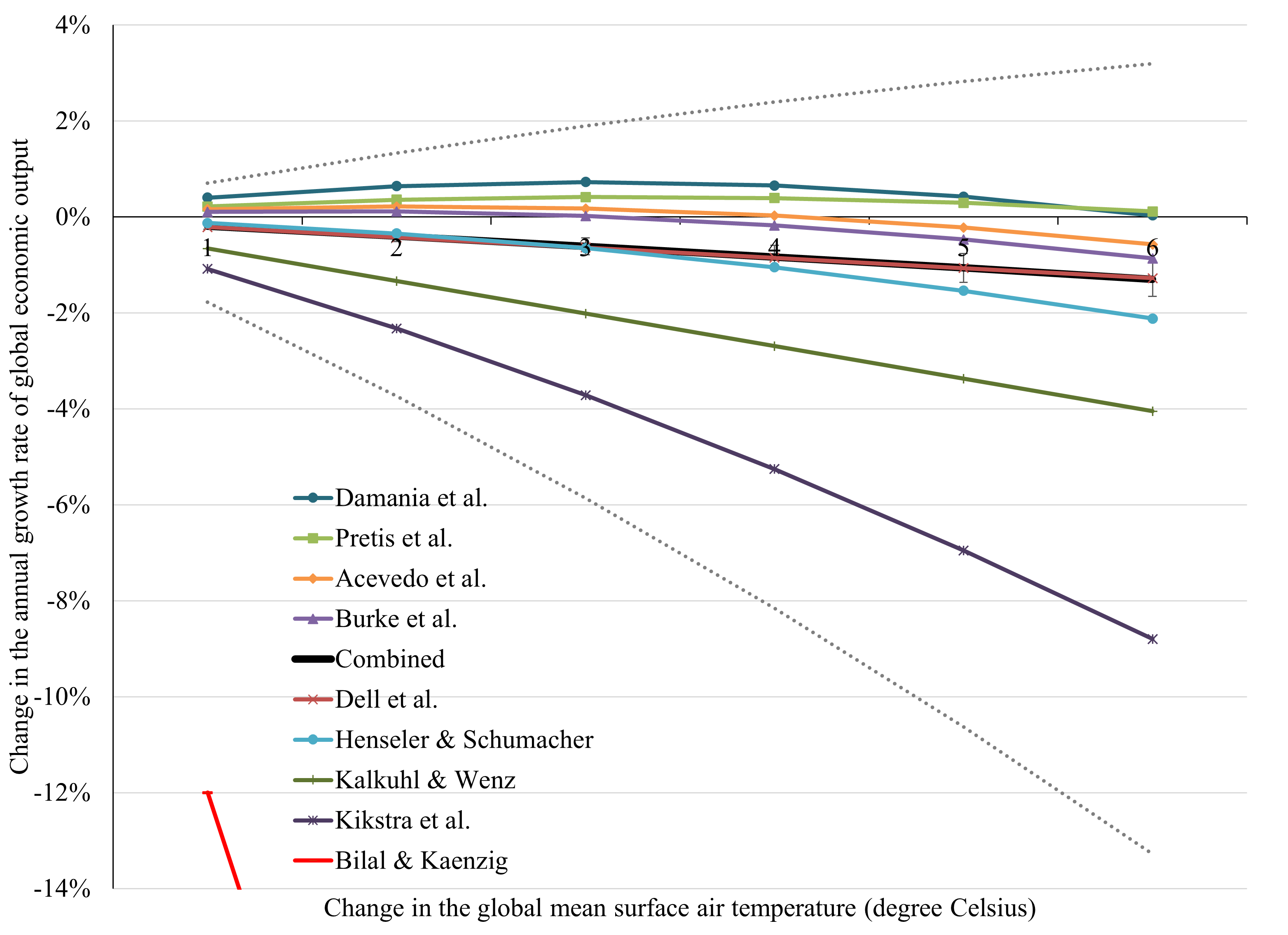

A recent paper by Adrien Bilal and Diego Kaenzig attracted a lot of attention. They find that 1K global warming would cut average income by 12%. They claim that this estimate is six times larger than previously thought, but is more like sixteen times larger when compared to whole literature rather than their selective citations.

I updated Figure 2 in that paper:

How do they get there? The main regression yields a Jorda-like impulse response function. They regress the growth rate of per capita income, averaged over one to ten years, on temperature. This is a Dell-like specification. The regression is unbalanced: A flow is regressed on a stock. This works in-sample as fixed-effects compensate for the imbalance. As a result, the fixed-effects are correlated with the variable-of-interest, which hampers interpretation. Fixed-effects do not help out-of-sample so that models like this do not cross-validate.*

If economic growth depends on the level of temperature, then growth will be permanently higher or lower if climate stops changing. Use this model for deep history and you’ll find that poor countries are poor because they are hot. This is the sort of climate determinism that would make Ellsworth Huntington blush.

In this, Bilal and Kaenzig repeat the mistakes of Dell, Burke, and Wenz. They add a twist, which explains why they are even further out. Instead of using temperature, Bilal and Kaenzig use temperature shocks, which they define as temperature deviating from its recent trend. In the period from 1950 to 2023, temperature shocks fall between -0.2K and +0.2K. That is, their central forecast — 12% for +1K — is five times larger than their largest observed shock. I once, unsuccessfully, tried to coin the term “ultrapolation” for what lies beyond extrapolation.

The temperature shocks of Bilal and Kaenzig look remarkably like El Nino / Southern Oscillation.** The economic effects of ENSO have been studied extensively. It is damaging because normal weather patterns are disrupted for a short time. Climate change is different. It is permanent, giving people, companies, governments, institutions, and technologies time to adapt to the new circumstances. As too many others before them, Bilal and Kaenzig estimate a short-term elasticity and confuse it for a long-term elasticity.

*Update: Bilal and Kaenzig also estimate a model without fixed-effects. The results are roughly the same. That misses the point, though. Whereas Burke uses fixed-effects to rebalance a misspecified equation, Bilal and Kaenzig uses local trends for the same purpose. This works fine in-sample but not out-of-sample. For this model to work out-of-sample, they would have to re-estimate their local trend for every realization of a stochastic model of future temperatures. Section 4.2 reveals that they do not do this.

**Update: In the November 2024 version of the paper, Bilal and Kaenzig add a control for ENSO to their main specification. This has little effect. This is hardly surprising. If their temperature shocks look remarkably like ENSO, then adding ENSO as a control does not add new information.